SIP vs PPF For Child’s Future: Which Investment Option Can Create A Bigger Long-Term Corpus?

SIP vs PPF: All parents want financial security for their child’s future. With the escalating costs of education and with professional courses and future milestones such as higher studies, career planning or marriage, long-term financial planning has become more important than ever. Inflation means prices increase year after year, and just putting money in a bank account may not be enough to build a strong financial cushion for your child.

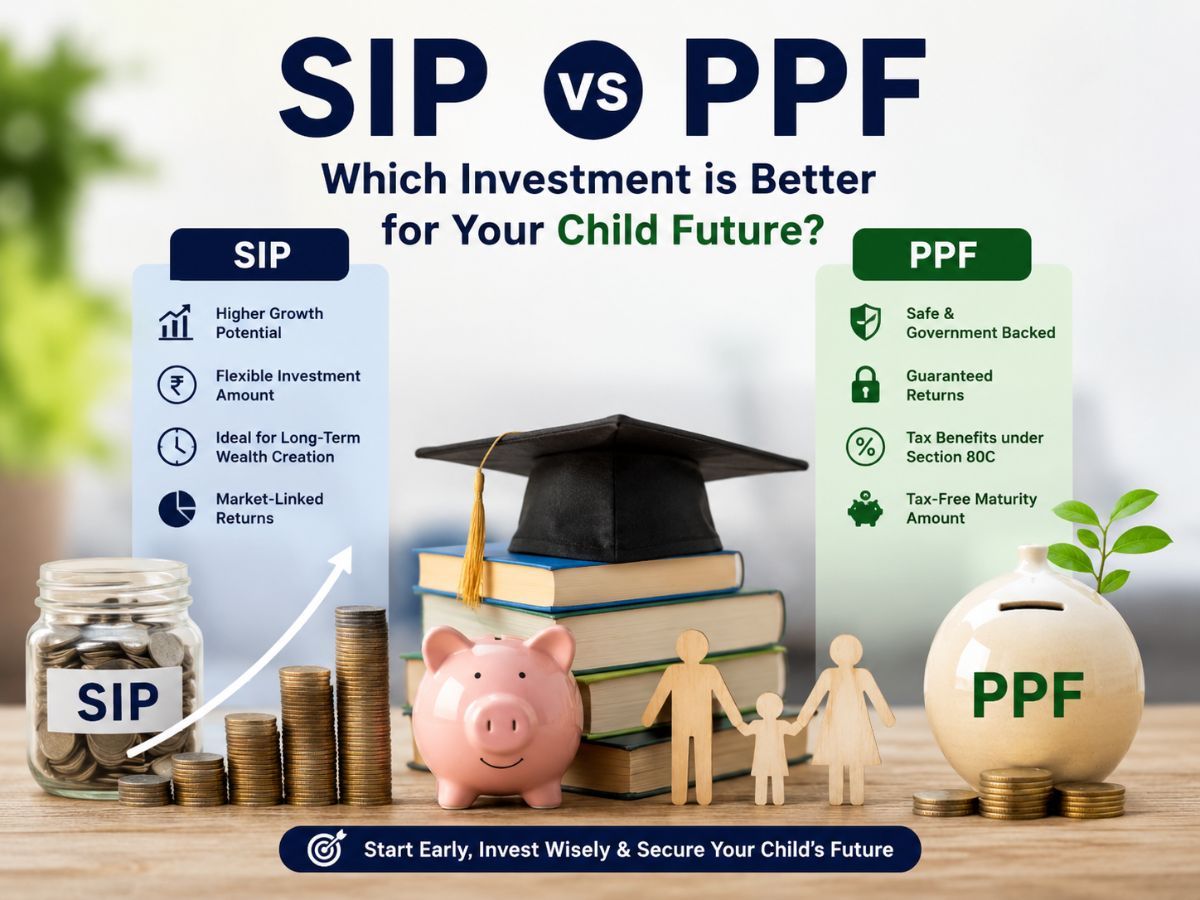

Hence, a lot of parents are looking for disciplined investment options like SIPs and PPFs to accumulate wealth in the long term. Both encourage you to invest regularly and can help your savings to grow over time. But these are very different in their working. SIPs are linked to the market’s performance and provide a higher probability of growth. PPF offers guaranteed returns supported by the government.

The real question is, do you want growth potential or guaranteed stability?

SIP, or systematic investment plan, is the process of investing a fixed amount of money in mutual funds on a periodic basis. This is usually done on a monthly basis.

SIPs help in wealth creation over a period of time and also reduce the burden of timing the market as against investing a lump sum amount. SIPs also benefit from rupee cost averaging and compounding, which can create large wealth over the long term.

One of the biggest reasons why many young investors prefer SIPs is flexibility. You can start with just ₹100 a month and increase the amount as your income grows. You don’t have to put a big chunk of money down to start.

SIPs also provide the opportunity for better long-term returns, especially when invested for a goal such as children’s education or wealth creation in the future. Since the money is invested periodically over a period of time, SIPs can also help in beating inflation and creating a bigger corpus over the long term.

SIPs are invested in either equity or hybrid mutual funds, and therefore, the returns are market-dependent.

Over a long-term horizon, equity mutual funds have outperformed other traditional savings products.

The public provident fund frontier is a concept in economics which represents the maximum possible combinations of two different goods which can be produced using a given level of resources and technology.

PPF is a government-backed long-term savings instrument to create wealth and for tax-saving purposes.

PPF has a 15-year lock-in and is giving an interest rate of 7.1% for the FY 2025-26.

Returns are fixed, compounded annually and completely tax-free.

Conservative investors love the PPF because of its safety and stability. It is supported by the government, and hence, investors don’t have to worry about market volatility and sudden losses.

Offers assured returns and tax benefits under section 80C The maturity amount is tax-free. PPF is often seen as a stress-free and dependable way to save for families with long-term goals such as retirement or a child’s future.

Market Fluctuations And Capital Protection: PPF is generally preferred by those investors who want to avoid market fluctuations.

| Parameter | SIP | PPF |

|---|---|---|

| Nature | Market-linked investment | Government-backed savings |

| Returns | Market-dependent | Fixed at 7.1% |

| Risk | Moderate to high | Very low |

| Investment Amount | Starts from ₹100 | ₹500 to ₹1.5 lakh annually |

| Lock-in | Depends on fund type | 15 years |

| Liquidity | Higher | Limited |

| Taxation | LTCG/STCG applicable | Tax-free returns |

| Best For | Wealth creation | Stable long-term savings |

This is where SIPs often excel.

If you are looking at a longer-term horizon like your child’s higher education in 15-20 years, SIPs have traditionally provided inflation-beating returns. Equity mutual funds can provide double-digit annualised returns over long periods of time, helping parents build a much larger corpus.

PPF, however, provides predictability and security but may not be able to beat inflation by a big margin over very long periods.

Here is an example for better understanding:

Now, let us consider an example where a parent begins to invest 5,000 per month for 15 years:

A SIP which is expected to yield returns of 12% per annum is likely to create a corpus of over Rs 25 lakh.

PPF at 7.1% can give around Rs 16-17 lakh.

And the longer the time, the bigger the gap, thanks to the power of compounding.

When SIP might be a better fit:

You are investing for the long term.

You are able to accept short-term swings in the market

Your goal is to build wealth

You want returns to trail inflation

You have future goals that are expensive, like studying abroad

PPF can be a good option for investors who:

Prefer some profit

Doesn’t want market risk

Tax Saving the Smart Way

Looking for sustained, steady growth

Preserve capital rather than aggressive growth

Financial experts often say the best way may be not one or the other, but a combination of the two. A combination could be adopted in a manner to gain the safety of PPF and growth benefits of SIPs.

PPF may ensure your safety and secure savings, while SIPs can assist you to create a larger inflation-adjusted corpus. This combination might build a balanced portfolio for the child’s future.

At the end of the day, it comes down to your financial goals, your risk appetite and the kind of financial future you’d want your child to have.

SIPs can have a better growth potential if you are looking at wealth creation and beating inflation over the long term. For a safe, guaranteed and tax-efficient investment, PPF still remains among India’s most trusted schemes.

For many families, the best strategy may be to use both in tandem to balance growth and security as they prepare for the rising cost of education and expenses down the road.

Priyanka Roshan is a business writer and assistant editor at the NewsX website who tracks everything from stock market swings and corporate earnings to personal finance trends and policy shifts. Known for turning fast-moving business developments into sharp, reader-friendly stories, she combines speed, accuracy, and a data-driven approach to break down complex financial news for everyday audiences.

With over 9.5 years of newsroom experience, Priyanka has worked with leading media organisations, including Moneycontrol, Times Now, and Ping Digital, covering diverse beats such as business, politics, technology, auto, travel, sports, and the world. From live breaking news desks to SEO-led digital storytelling, she specialises in creating engaging content that keeps readers informed without overwhelming them.

United States National Team FIFA World Cup 2026: Squad, Ranking, Key Players & Full Preview

Learn about the United States national football team FIFA World Cup 2026 squad, FIFA ranking,…

Controversy Erupts In Reasi Over Eid-ul-Adha Greeting Post Shared On Social Media By A School

Presentation Convent High School in Jammu and Kashmir’s Reasi district sparked controversy after sharing an…

Who is DK Shivakumar? Congress veteran to replace DK Shivakumar as Karnataka CM

Congress leader D. K. Shivakumar is likely to replace Siddaramaiah as Karnataka Chief Minister amid…